In the second trade note published in his ongoing Strategy Series, Thomas Browne demonstrates from first principles how Eris Swap Futures track the P&L of underlying interest rate swaps.

The paper further shows that the Eris price more accurately reflects the total return of a swap than comparing changes in par swap rates.

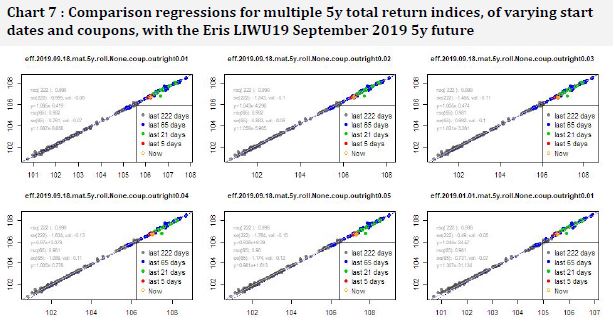

Finally, using regression analyses, Browne proves that even with different coupons and start dates, Eris Swap Futures can provide equivalent market exposure and substantially the same economic return as an IRS, acting as a highly effective replacement for OTC swaps.

Click here to request the full white paper.

Date