In the first trade note of his Strategy Series, Thomas Browne provides a detailed introduction to Eris Swap Futures, put into context with Eurodollar futures and OTC interest rate swaps.

- Eris Swap Futures can provide higher duration exposure than other fixed income futures, including convexity, making for a more natural fit for longer dated fixed income trading

- Compared to OTC IRS, Eris offers concentrated liquidity using IMM dates, futures margin benefits, greater accessibility, and efficiency of unwinds

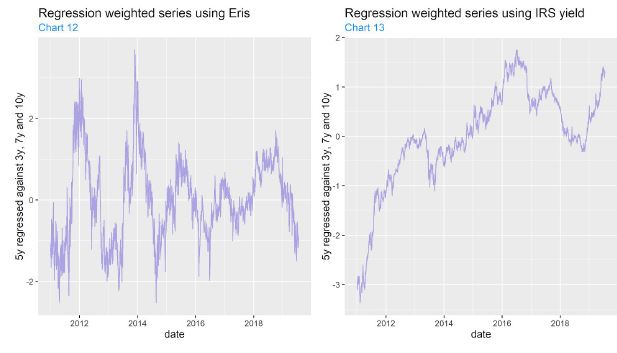

- Eris Swap Futures, quoted in price and tracking total return, can allow for more simple mean reversion trading opportunities than OTC swaps with weights calculated using only yield

Click here to request the full white paper.

Date