CME Group unveils Eris Options contract specifications

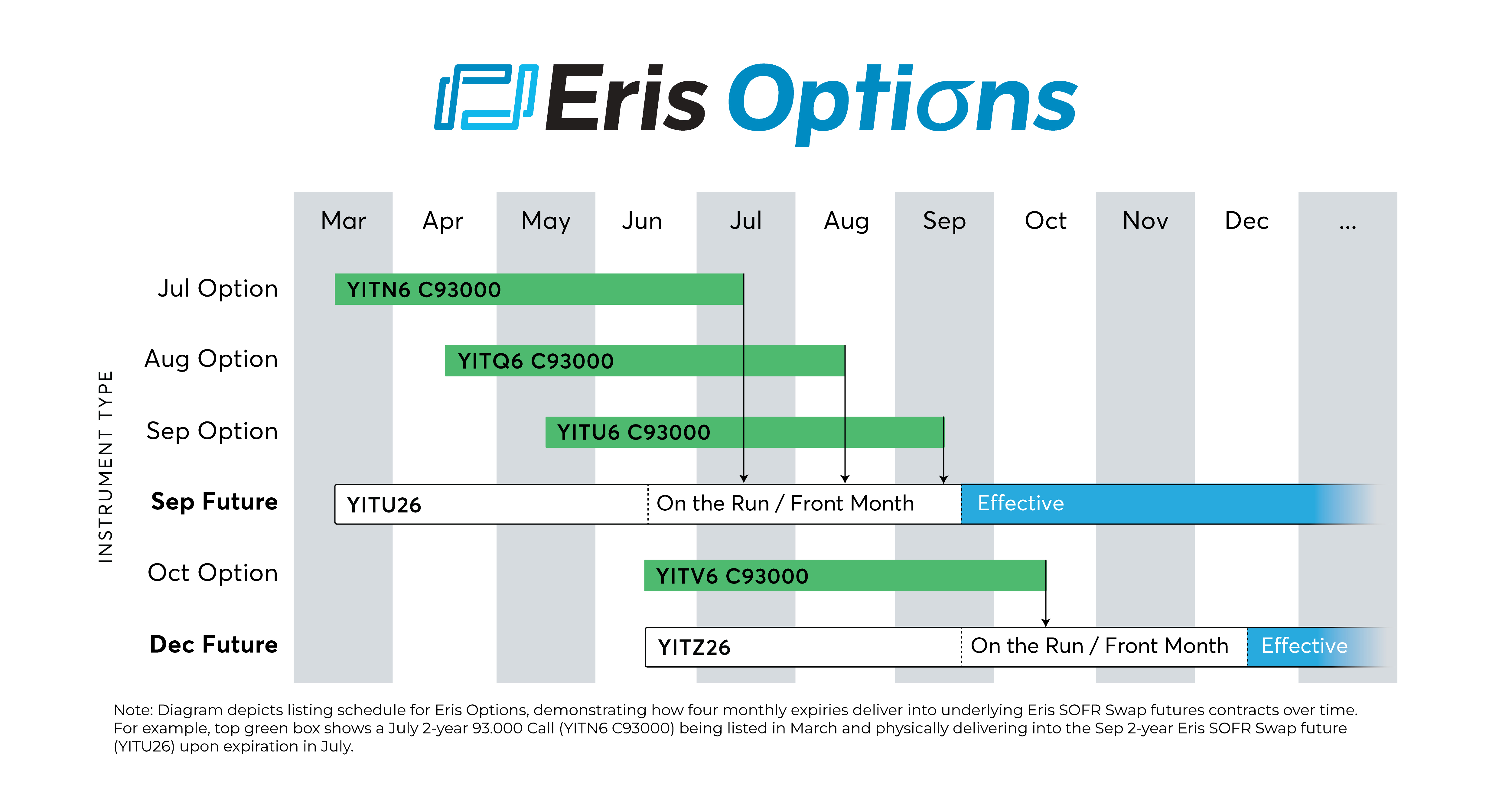

Note: Diagram depicts listing schedule for Eris Options, demonstrating how four monthly expiries deliver into underlying Eris SOFR Swap futures contracts over time. For example, top green box shows a July 2-year 93.000 Call (YITN6 C93000) being listed in March and physically delivering into the Sep 2-year Eris SOFR Swap future (YITU26) upon expiration in July.

- Following the recent press release announcing the June launch of Eris Options, CME Group released the Eris Options 2-page tearsheet, which includes detailed contract specifications

- Eris Options offer swaption-style risk in listed CME Group options, with four consecutive European-style monthly expiries (e.g., Jul, Aug, Sep, Oct) that physically deliver into 2-year, 5-year, or 10-year Eris SOFR Swap futures

- Eris Options feature futures-style margining, similar to forward-premium OTC swaptions

- They remove operational burdens associated with swap data repository (SDR) reporting, uncleared margin rules (UMR), and manual trade confirmations

- For more information, visit erisfutures.com/options

New Eris SOFR Market Maker: Bank of Montreal

- The BMO swap desk is the most recent dealer to start responding to inquiries for Eris SOFR block trades

- “We are pleased to respond to the growing end user demand for Eris SOFR Swap futures by providing block trade liquidity across the swap curve,” said Akash Agrawal, Head of US Rates, Bank of Montreal

- Futures brokers can contact Akash Agrawal, Wesley Hyde, or Mike Novack on Bloomberg IB chat, and BMO clients can contact their BMO sales coverage

- Click here for a full list of Eris SOFR Block Market Makers

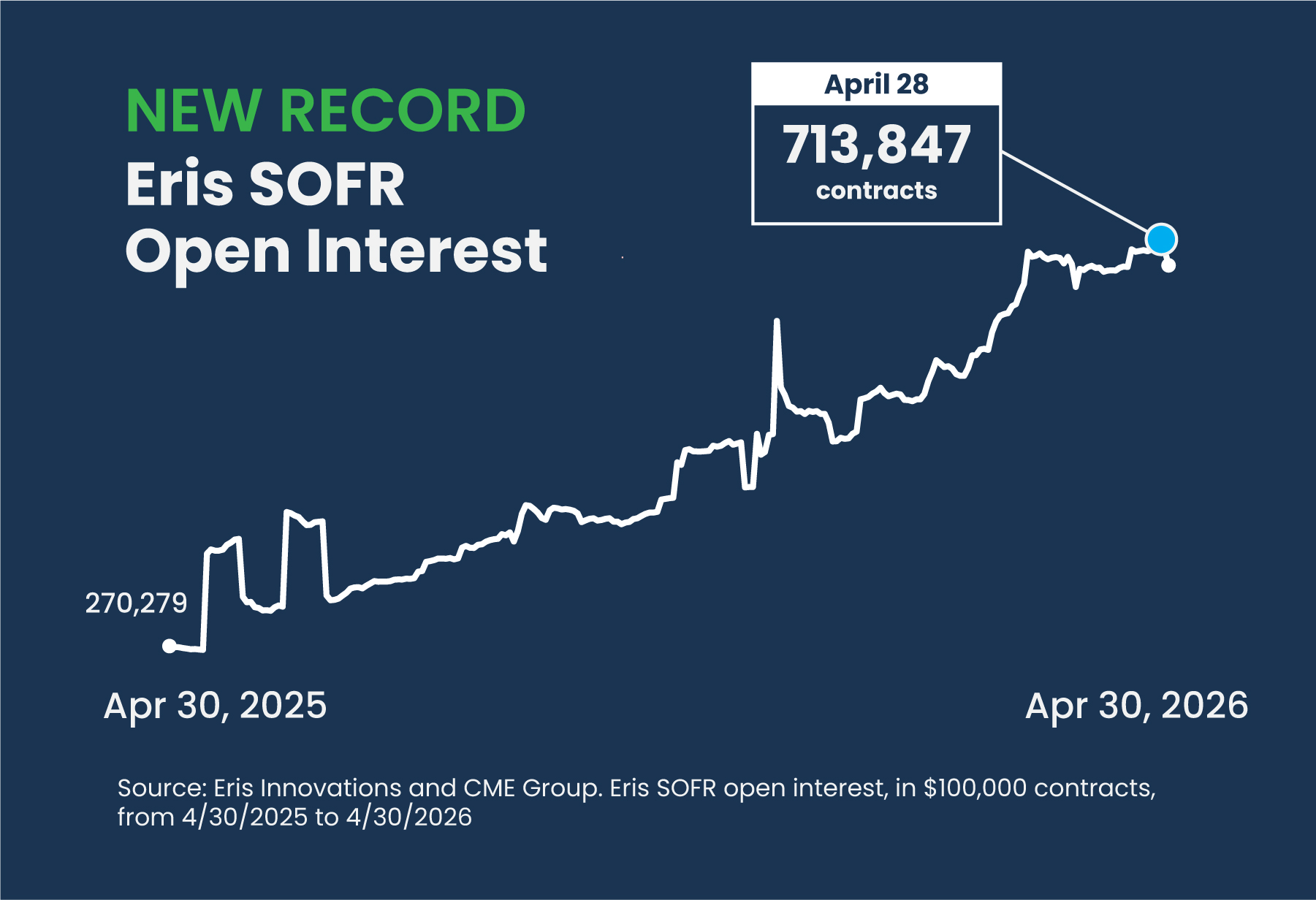

Open interest cracks 710,000 contracts

- Eris SOFR Open interest (OI) reached 713K contracts ($71B notional) on Apr 28, finishing the month at 697K contracts

- OI in Eris SOFR Swap futures tripled over a 16-month period from January 2025 to April 2026, increasing from 242,000 to the recent high of 713,000 contracts

- OI leapt 158% year-over-year (YoY), up 427K contracts ($42.7B notional) from April 2025

- Mega blocks boosted OI including three Apr 17 trades, each greater than 7,500 contracts ($750mm notional)

- April activity follows record Q1 daily volume of 22,000 contracts, and record March daily volume of 44,000 contracts

New CME Group article: Unlocking Capital with Eris SOFR

- Eric Leininger of CME Research and New Product Development released a new article on reducing capital with Eris SOFR Swap futures

- It begins, “In the current landscape of shifting interest rate cycles and tightening liquidity, institutional hedgers are facing a silent drain on their balance sheets: initial margin (IM).”

- It notes, “the era of set-and-forget OTC hedging is over. As capital costs remain elevated, the ability to reduce margin …by 60% is a competitive necessity.”

- For similar risk transfer, insurers, banks, and asset managers achieve more capital flexibility with less balance sheet drag

- Explore initial margin comparisons between Eris SOFR and cleared OTC swaps at erisfutures.com/marginsavings

Date