Eris Public File Server

Eris Innovations provides intraday and end of day contract pricing data on its ftp site. This guide explains the data and files available.

Browser Access

Use the following URL to access Eris files through a browser window:

Individual files may require a username (“anonymous”) and password (“anonymous”). The FTP folder contains both daily "date" named files, a most recent daily "latest" named version, and intraday “live market” files. Every 3 months, daily "date" named files are archived to an archive folder, structured by year and month: https://files.erisfutures.com/ftp/archives/

For questions or more information, please contact questions@erisfutures.com

Eris Options

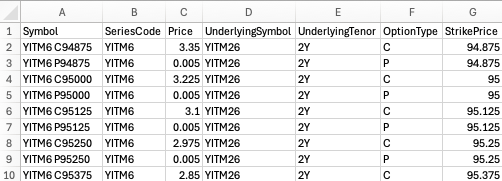

FILES

- Intraday and final settlement prices for all options

- File includes option price, volatility, options analytics and contract reference data

- Eris_Options_[yyyymmdd]_IntradaySettles.csv (Available ~11.45 am ET)

- Eris_Options_[yyyymmdd]_Settles.csv (Available ~03:15 pm ET)

- File layout:

Eris SOFR Swap Futures

Files & Pricing Data

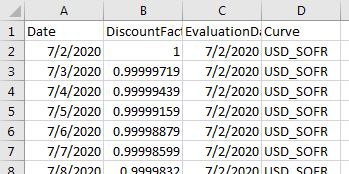

- Discount factor curves, today to 50 years, for SOFR markets

- EOD curves are calibrated to reprice observed mid/traded prices of Eris front contracts at 15:00 ET daily, used in forecasting and discounting all future cash flows, and from which all Eris contracts are priced and settled

- Intraday curves are calibrated to reprice live observed order book mid-prices of Eris contracts during regular trading hours

- Eris_[yyyymmdd]_EOD_DiscountFactors_SOFR.csv (Available ~15:40 ET)

- Eris_Latest_EOD_DiscountFactors_SOFR.csv (Updated ~16:20 ET)

- Eris_Intraday_DiscountFactors_SOFR.csv (RTH, every 5 mins)

- RTH means Regular Trading Hours

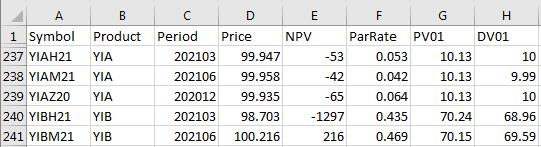

- Theoretical live intraday, preliminary settlement and final settlement prices for all contracts

- File includes contract reference data, contract price, price components (Eris A-swap NPV, B-past fixed and floating coupons, and C-Eris PAI), PV01/DV01 and current coupon accrual data

- Eris_Instruments_[yyyymmdd]_PrelimSettles.csv (Available ~15:20 ET)

- Eris_Instruments_[yyyymmdd]_Settles.csv (Available ~15:40 ET)

- Eris_Instruments_Latest_Settles.csv (Updated ~16:20 ET)

- Eris_Standards_Pricing_Intraday.csv (RTH, every 5 mins)

- The live intraday data is also available using the Eris MS Excel Addin, outlined in the section below, titled “Live Intraday Price Retrieval with Eris MS Excel Add-in”

- File layout:

- Often also referred to as Eris PAI files

- Source files for accrued values — past fixed and floating coupons and PAI — prior to final settlement prices

- Published twice daily; first on T-1, before SOFR is published for T, and then again on T, after SOFR is published

- Eris_Instruments_[yyyymmdd]_Prices_Prev_PAI_Rate.csv

- Available ~15:40 ET on T-1 (trade date prior to yyyymmdd)

- Prices of all contracts, with past coupons and PAI updated to the current trade date, with the latest PAI accrual occurring at the PAI rate (SOFR) of the previous trade date (as SOFR for current trade date not yet published)

- Eris_Instruments_[yyyymmdd]_Prices_TopDay_PAI_Rate.csv

- Available ~08:10 ET on T (trade settle date yyyymmdd)

- Prices of all contracts, with past coupons and PAI updated to the current trade date, re-run following the publication of the PAI rate (SOFR) for the current trade date

- File Layout:

- Key Data Locations

- Past payments of fixed and floating coupons found in column AD

- Eris PAI found in column AE

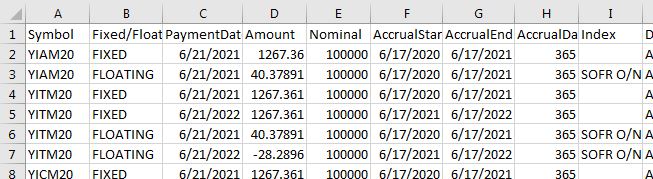

- Future fixed and forecasted floating cash flows of all contracts

- Includes forecasted floating rates, coupon accrual start and end dates, payment dates and discount factors

- SOFR in the filename represents SOFR discounting

- Eris_[yyyymmdd]_EOD_PricedSwapLegAnalysis_SOFR.csv (Available ~15:40 ET)

- Eris_Latest_EOD_PricedSwapLegAnalysis_SOFR.csv (Updated ~16:20 ET)

- The Eris Pricing Engine® (PE) calibrates discount factor curves that are used to settle all Eris contracts. These discount factor curves are used to imply spot starting SOFR swap rates, published as follows:

- Eris_[yyyymmdd]_EOD_ParCouponCurve_SOFR.csv (Available ~15:40 ET)

- The Eris PE also runs live, generating theoretical intraday prices for all Eris contracts and spot starting swap rates implied by the Eris curve. Eris spot starting swap rates are contributed to Bloomberg and may be retrieved using Bloomberg’s generic swap codes, attributed with “Eris”; Bloomberg Terminal syntax:

- Spot starting 1-30yrs O/N SOFR swap, e.g. {USOSFR2 ERIS Curncy GO}

- The live theoretical intraday Eris prices and Eris implied spot starting swap rates may also be pulled into an Excel spreadsheet using the Eris MS Excel Addin function library, details below

- Eris provides a free MS Excel Addin function library, which facilitates the retrieval of real-time and reference data for all Eris Swap Futures contracts and implied spot starting swaps

- Data includes contract swap terms, Eris price components (A/B/C’s), live order book prices, theoretical mid prices for contracts without order book prices, contract risk parameters, par equivalent swap rates of Eris contracts, and many more data points

- More information and download instructions available here

- ErisMarketsAddin.xlam (Static file)

- Historical time series of prices and price components (A/B/C’s) for all Eris contracts from December 2012 to present

- Eris_Historical_Prices.csv (Updated ~08:10 ET)

- Schedule of US Govt Securities, Sifma & UK holidays going out 40 years, used in calculations

- Eris_[yyyymmdd]_EOD_Holidays.csv (Available ~15:40 ET)