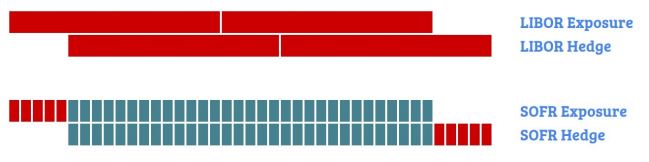

In the fourth trade note of his ongoing Strategy Series, Thomas Browne explains how the transition from periodic (1, 3, 6 month) LIBOR fixings to daily SOFR removes the reset risk typically associated with hedging with futures. Browne then makes the case that standardized futures are better suited to hedging in SOFR given less need for customization, concentration of liquidity, and lower margins, among other benefits.

Date